Featured

Table of Contents

The score is as of Aril 1, 2020 and is subject to transform. Haven Life And Also (Plus) is the advertising and marketing name for the Plus cyclist, which is included as component of the Place Term policy and offers access to added solutions and benefits at no price or at a discount.

Find out more in this overview. If you depend upon someone financially, you may ask yourself if they have a life insurance policy. Discover how to discover out.newsletter-msg-success,. newsletter-msg-error display screen: none;.

There are several kinds of term life insurance policy plans. Instead of covering you for your entire lifespan like entire life or global life plans, term life insurance coverage only covers you for an assigned amount of time. Policy terms usually vary from 10 to 30 years, although shorter and longer terms might be available.

Many typically, the policy expires. If you want to preserve coverage, a life insurance firm might offer you the option to renew the policy for one more term. Or, your insurance company might permit you to transform your term strategy to a long-term policy. If you added a return of costs cyclist to your plan, you would certainly get some or all of the money you paid in premiums if you have outlasted your term.

What is a simple explanation of Level Death Benefit Term Life Insurance?

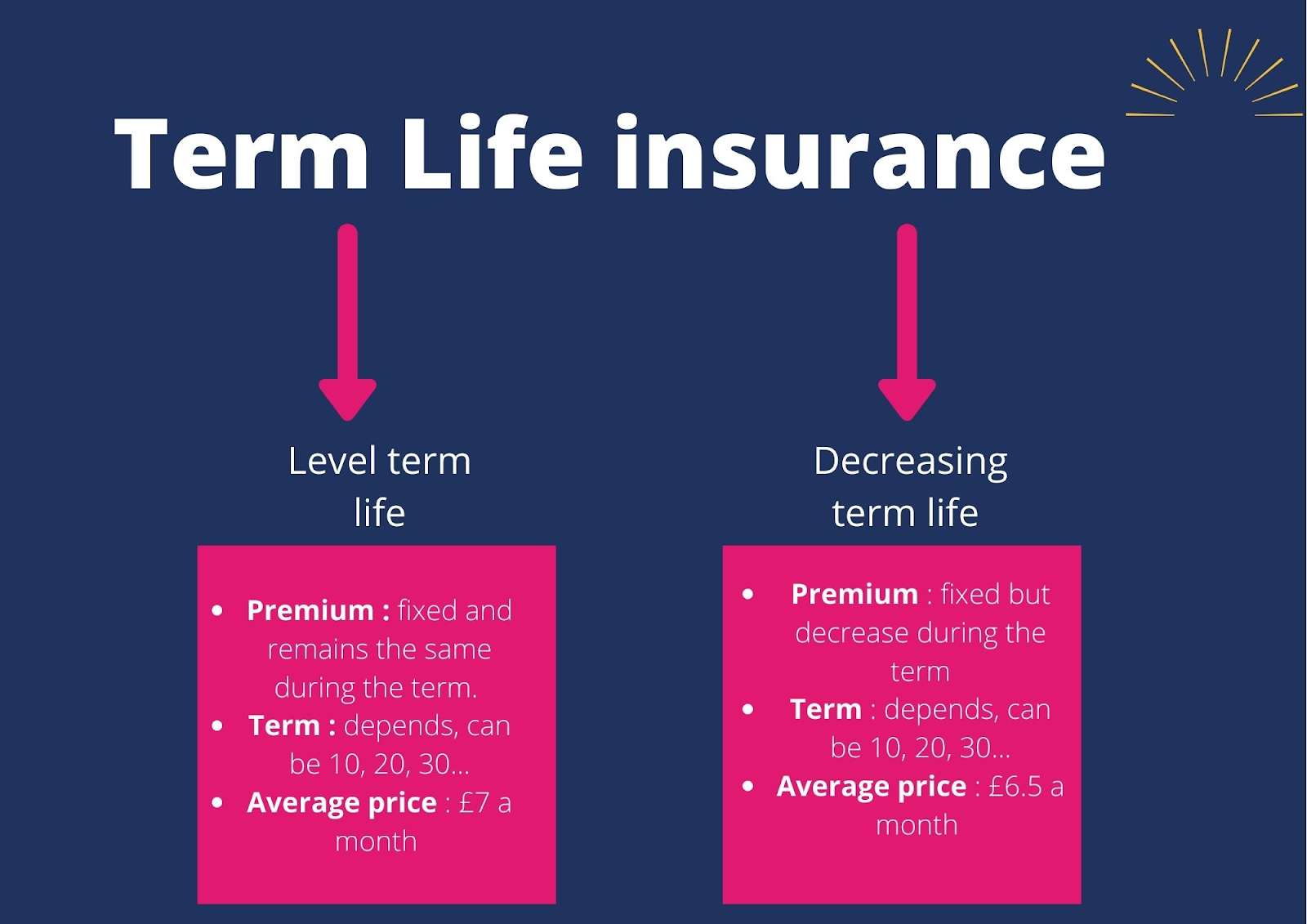

Level term life insurance policy might be the most effective choice for those who want insurance coverage for a collection amount of time and desire their costs to remain stable over the term. This might use to consumers concerned about the affordability of life insurance coverage and those who do not intend to transform their death advantage.

That is due to the fact that term plans are not assured to pay out, while irreversible plans are, gave all premiums are paid., where the death benefit lowers over time.

On the other hand, you might be able to secure a less expensive life insurance rate if you open up the policy when you're more youthful - No medical exam level term life insurance. Comparable to advanced age, inadequate wellness can additionally make you a riskier (and more expensive) candidate for life insurance. However, if the problem is well-managed, you may still have the ability to discover economical insurance coverage.

Health and age are usually much more impactful costs elements than gender., may lead you to pay even more for life insurance policy. High-risk jobs, like window cleaning or tree cutting, may additionally drive up your cost of life insurance coverage.

Is 20-year Level Term Life Insurance worth it?

The very first action is to establish what you require the plan for and what your budget plan is. Some companies provide on-line pricing estimate for life insurance policy, but numerous need you to speak to an agent over the phone or in individual.

The most prominent type is currently 20-year term. Most business will certainly not market term insurance to a candidate for a term that ends past his or her 80th birthday celebration. If a plan is "sustainable," that implies it continues in force for an added term or terms, up to a specified age, even if the wellness of the insured (or other variables) would create him or her to be denied if she or he got a new life insurance policy.

Costs for 5-year eco-friendly term can be level for 5 years, then to a new rate reflecting the new age of the insured, and so on every 5 years. Some longer term policies will guarantee that the costs will not enhance during the term; others do not make that warranty, enabling the insurer to increase the rate throughout the plan's term.

This implies that the policy's proprietor can alter it into a long-term sort of life insurance coverage without extra evidence of insurability. In many kinds of term insurance coverage, consisting of house owners and vehicle insurance policy, if you haven't had a claim under the plan by the time it expires, you get no refund of the costs.

Who offers Best Value Level Term Life Insurance?

Some term life insurance policy customers have actually been miserable at this end result, so some insurers have developed term life with a "return of costs" attribute. The premiums for the insurance coverage with this function are typically significantly greater than for policies without it, and they generally require that you maintain the policy effective to its term otherwise you waive the return of premium benefit.

Level term life insurance coverage costs and fatality advantages stay regular throughout the policy term. Level term life insurance is commonly much more inexpensive as it doesn't build cash worth.

While the names usually are used reciprocally, level term coverage has some important distinctions: the premium and death benefit stay the same for the period of coverage. Degree term is a life insurance policy plan where the life insurance policy premium and survivor benefit remain the exact same throughout of protection.

These plans can last for a 10-year term, 15-year term, 20-year term or 30-year term. The size of your protection duration may depend on your age, where you are in your job and if you have any type of dependents. Like various other sorts of life insurance policy coverage, a degree term policy offers your beneficiaries with a death advantage that's paid out if you die throughout your coverage duration.

What is the process for getting Level Term Life Insurance Rates?

That commonly makes them an extra cost effective option permanently insurance policy protection. Some term policies may not keep the premium and survivor benefit the very same in time. You do not wish to wrongly believe you're acquiring level term coverage and after that have your survivor benefit change later. Many individuals obtain life insurance policy protection to aid economically secure their loved ones in instance of their unexpected fatality.

Or you might have the choice to convert your existing term insurance coverage right into an irreversible policy that lasts the rest of your life. Numerous life insurance plans have prospective advantages and downsides, so it is very important to recognize each before you determine to acquire a policy. There are numerous benefits of term life insurance, making it a popular option for coverage.

{kind=link}

Latest Posts

Instant Insurance Life Smoker

Final Care

Universal Life Insurance And Instant Quote